{kind=link}

HM Revenue and Customs (HMRC) has vigorously denied claims that its new Employment Status Service tool is unreliable and inaccurate.

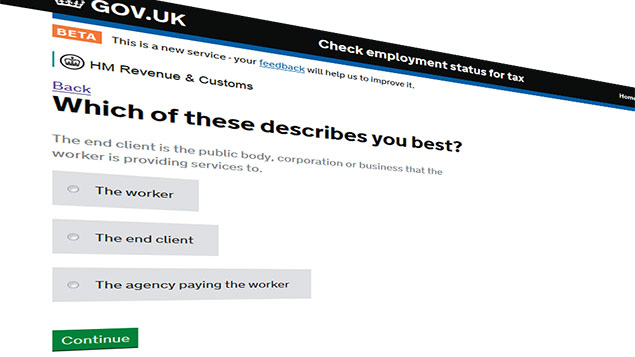

HMRC released the online tool last week as a way to help organisations decide whether public-sector workers fall under IR35 tax legislation.

It comes in advance of new rules for intermediaries, introduced to the public sector next month, which shift the responsibility for ensuring that people who work via a limited company pay the right level of tax and national insurance from the individuals themselves to employers and agencies.

Employment status resources

HMRC has come under increased pressure from contractors and employers to make the tool available before the 6 April start date.

Concerns have already been raised that the intermediaries legislation could lead to a drain on talent, with reports suggesting that public-sector contractors with in-demand skills such as IT are already looking to move to the private sector for more favourable tax terms.

Contractors or those who engage them can use the tool to answer a pre-programmed series of questions, which change depending on the user’s responses.

However, some contractor services companies have suggested that the results provided by the tool may not be reliable or will leave contractors unsure of their status.

One contractor portal, ContractorCalculator, claims it has trialed the tool by inputting 21 historical court cases around employment status.

More than a quarter of cases received an “unknown” result, while one-tenth “passed” the online test (meaning they would fall outside of IR35), despite a judge having decided otherwise.

It also found that contractors who are “significantly controlled” and moved about frequently tended to pass the online test, despite case law indicating this would not be the case.

Another contractor company, Qdos Contractor, came to a similar conclusion. CEO Seb Maley said that the tool could have a long-term impact on how public-sector organisations engage with contractors and could lead to many contractors moving to the private sector for ms.

He said: “From a first examination, this test is largely reliant on substitution. If, as a contractor, you don’t have the right to send a replacement, there is little prospect of the tool deeming you outside IR35, even if you have control over how the work is done.

“The consequences of mistakenly placing a contractor inside or outside IR35 are huge for all concerned.”

Dave Chaplin, CEO of ContractorCalculator, raised concerns that an “unknown” status could create uncertainty: “Not only does it not mean anything, but the tool gives a significant number of contractors an ‘unknown’ status. Claiming they will stand by this is hardly pioneering work and does not provide the certainty to the market which was their original goal,” he said.

Chaplin said many of the questions failed to offer much direction in “mutuality of obligation”, which is one of the key tenets in determining employment status.

“With only a few weeks to go before the IR35 reforms come into force, HMRC’s tool is nowhere near fit for purpose and HMRC could be handing out employment status decisions to contractors, agencies and public-sector hirers that are wrong – or simply leaving them in limbo land,” he added.

Maley echoed these concerns: “IR35 is a complex issue. It takes expertise and the ability to look at each case individually to be confident of an accurate decision. It’s hard to see how a one-size-fits-all approach like this can be completely reliable.

Like all tax changes, we are monitoring their effect to make sure they work effectively and fairly and we have yet to see any cause for concern.” – HMRC spokesperson

“With little time until changes to IR35 in the public sector are enforced, it’s concerning that HMRC’s new tool has only just been released. Changes are imminent, and there isn’t much time to iron out any teething problems.”

But HMRC strongly refuted the claims. A spokesperson said: “None of these claims is correct. The tool is working correctly and has been extensively tested. We welcome feedback from users.”

“Public-sector organisations and contractors are free to work with each other in a manner that suits their circumstances, however it’s fair that two people doing the same job should pay the same taxes. These reforms will help ensure that happens.

“Like all tax changes, we are monitoring their effect to make sure they work effectively and fairly and we have yet to see any cause for concern.”

Holly Cudbill, associate solicitor in the employment team at Coffin Mew Solicitors, said the concerns about the accuracy of the tool were “entirely valid”, however.

“Previously, HMRC published a checklist as guidance for whether a person was self-employed for tax purposes. This was criticised as it gave an indication of employment status, but no definitive answer.

“The difficulty with the new online tool is exactly the opposite. While the new tool does give a definitive answer (albeit in some cases the answer is, definitively, ‘unknown’), it is wholly dependent on the prescribed boxes being ticked by the person using the tool.

“Given that a worker’s view of the working arrangement could be substantially different from that of the end client, this could feasibly lead to the same arrangement being classed by the tool as both self-employed and employed.

“Fortunately for the Government, the tool makes it clear that HMRC will only stand by the results if it agrees with them.

“The difficulty with this test, and other online status tools, is that the law on employment status is nuanced and dependent on the facts in each case: it cannot simply be reduced to a box-ticking exercise.”

Dan Fawcett, managing associate at law firm Bond Dickinson, said that there was no cause for concern as to whether HMRC’s definition of employment status could influence any employment tribunal on employment status.

“It is possible for HMRC and an employment tribunal to come to different conclusions in the same case,” he explained.

Sign up to our weekly round-up of HR news and guidance

Receive the Personnel Today Direct e-newsletter every Wednesday

“This is due to some differences in the tests applied and the fact that there are three possible statuses under employment law (employee, self-employed and worker) whereas HMRC only recognises two (employee and self-employed).

He added that employment tribunals will take into account HMRC’s view when deciding whether an individual is an employee or worker, but pointed out that there are numerous reported cases in which the tribunal has found an individual to be an employee or worker where HMRC had concluded the same individual was self-employed.

1 comment

I have just done this test and there is a major error in how it interprets the answer to the question on substitution. Specifically if you answer that your company has NOT provided a substitute, the end assessment assumes that you HAVE made a substitution.

Comments are closed.